London, 11 March 2025 – Canopius Group, a leading international specialty and P&C (re)insurer, today announced its financial results for the year ended December 31, 2024.

Highlights include:

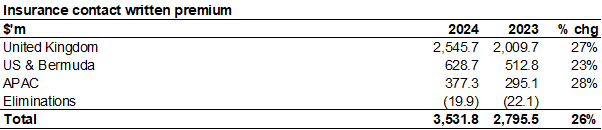

- Insurance Contract Written Premium increased 26% to $3.53bn (2023: $2.80bn)

- Profit after tax increased by 10% to $401.3m (2023: $363.4m)

- Tangible Net Asset Value (TNAV) increased by 25% to $1.81 bn (2023: $1.45bn)

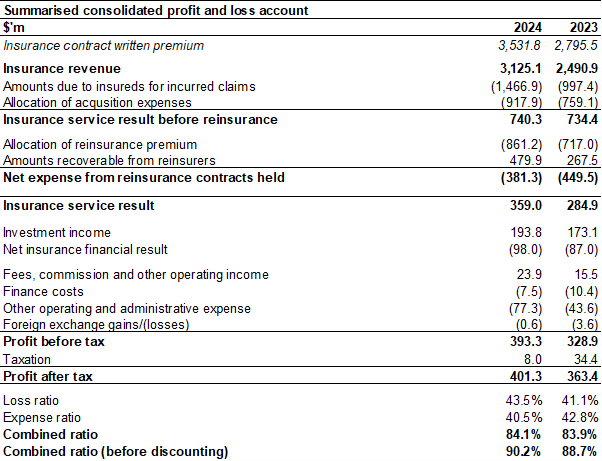

- Net insurance revenue increased 28% to $2.26bn (2023: $1.77bn)

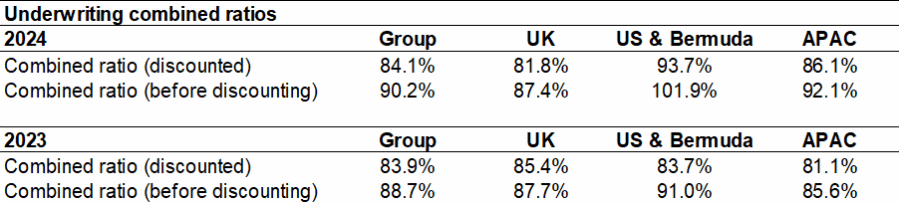

- Group net combined ratio (discounted) of 84.1% (2023: 83.9%)

- Group net combined ratio (undiscounted) of 90.2% (2023: 88.7%)

- Total net investment return of 5.4%, amounting to $193.8m (2023: $173.1m).

- Return on Opening Tangible Equity (ROTE) of 27.7% (2023: 32.0%)

Neil Robertson, Group Chief Executive Officer, said: “I am delighted with our 2024 results, achieving another record year of profitability. We have developed a consistent track record of returns and have the right framework, strategy and team to deliver profitable growth and attractive returns for our shareholders.

“Our strategy is to take an ambitious but disciplined approach to growing a sustainable international specialty and P&C (re)insurer in areas where we have or can have a distinction or competitive advantage.

“I am pleased to report another year of strong delivery against the goals we have set ourselves. While we expect 2025 to be a more challenging environment, we can look forward with confidence and are highly focused on building on our success and capitalising on the momentum we have achieved”.

Embedded our strategy and evolving our business

Our 2024 results are further testament to the transformation activities over the last three years, which continue to bear fruit.

There has been a substantial evolution of organisational disciplines stretching across the entire business. Decisive actions have been taken, the leadership team has been refreshed and strengthened, and we have been able to recruit top talent from across the industry.

We have been able to substantially re-define our risk appetite and strengthen our balance sheet, in the process reducing volatility in both income statement and balance sheet metrics.

We have also sharpened our strategic focus and reset our ambition towards structural growth over the next three years. We will continue to refine our competitive edge to further enhance and integrate our purpose, vision and innovation into all our activities. As our business grows and matures, we are committed to ensuring it remains efficient and, where practical, we will increase our underwriting commitments and expand our product offerings.

Reaping the rewards of a successful underwriting strategy

During 2024, the business has shown further strong progress. Once again, we have demonstrated the strength and versatility of our underwriting platforms, generating growth and profitability across the Canopius Group.

The underwriting portfolio has been repositioned towards higher quality and more diversified business. We are emphasising superior portfolio construction while also bringing in new underwriting talent and adding new product lines.

Our premium growth of 26% in the year added to the 22% growth that we saw in 2023 and again was very strong by both product and geography. Our attritional loss experience remains healthy, with good underlying accident year performance and positive prior year development.

Together these resulted in a record level of underwriting profitability, despite 2024 being an above average year for natural catastrophes by way of insured losses that have been seen globally throughout the year.

Demonstrating strong financial fundamentals

Our balance sheet is strong and has strengthened substantially again during the year, with tangible net assets growing by 25% to $1.81bn while our capital requirements have only grown by 13%. Our capital surplus over our capital requirements has therefore risen by 31% to $651.3m and continues to be robust, offering resilience to adverse events as well as strategic optionality.

In addition, we have a high-quality investment portfolio, with 73% of our core fixed income securities rated AAA/AA. Our reserving position is strong and has strengthened further during the year and we have limited legacy reserves (specifically back year U.S. casualty liabilities) through the purchase of a loss portfolio transfer in 2021.

Focusing on continued success in 2025

We have built an agile and resilient business, able to perform under a variety of market conditions. The start of 2025 has already thrown up several challenges and the loss environment and emerging rate pressure will continue to require strong disciplines going forward. Nevertheless, the year has started well for the Canopius Group, with attractive premium development and a good reinsurance renewal.

As expected, the broader rating environment remains dynamic, with multiple factors driving the rating environment. We are seeing some rate pressure, but we are relentlessly focused on pricing adequacy which is, in our view, the more refined and appropriate way to consider the impact on premiums. This continues to paint a positive picture across our portfolio.

We still believe there are many opportunities to improve and grow our business and we continue to be confident of the outlook for both for the coming year and into the future. Our priorities for 2025 are to implement our refreshed three-year plan, continue to focus on our successful underwriting strategy and philosophy, and build on our strong financial base.

– Ends –

Note: Unless otherwise stated, all figures are on IFRS 17 basis.

About Canopius

Canopius is an international specialty and P&C (re)insurer. Canopius underwrites insurance products on several platforms to offer a wide range of specialty solutions. Our offices are located in Australia, Bermuda, Singapore, the UK and the US. We underwrite through Lloyd’s Syndicate 4444 (managed by Canopius Managing Agents Limited), a US surplus lines insurer, Canopius US Insurance, Inc and Canopius Reinsurance Ltd, a Bermuda based Class 4 Reinsurer. By working together across regions, we create global insurance solutions in more than 130 countries.

For more information, visit www.canopius.com or linkedin.com/canopius

Group 2024 Financial Results commentary

Insurance Contract Written Premium (ICWP)

We have grown ICWP by 26% in the year with strong contributions across all our geographic segments. Rate has been less favourable in 2024 but was still positive across the portfolio (+1.2%). We have once again seen substantial organic growth across the Group.

In the UK, we are pleased once again to see strong growth, harnessing the benefits of the re-setting of our UK underwriting model in recent years. We have seen growth in Property Direct & Facultative (D&F), despite increased levels of competition, and in Reinsurance, where we have reset our growth ambitions in the last two years.

We have also benefitted from growth in Specialty lines, notably in Energy but also including Equine & Livestock, Accident & Health (A&H), Marine and Specie. In Professional Lines, due to more challenging market conditions, we were highly selective in our approach towards growing the portfolio.

One of the particularly bright spots was Portfolio Solutions, where from a near standing start, we have written nearly $300m of ICWP. We have captured business from five market facilities and continue to be excited about our prospects to develop this business further.

In the U.S. and Bermuda, where we continue to see attractive future opportunities, growth was fuelled largely by Property D&F, reflecting both strong demand and a firm rate environment. We continued to deliver growth in our cyber book, despite some challenges in a highly dynamic market and we also grew Canopius Re in both specialty and marine classes.

Like others in the market, we saw continued challenges in our Management and Professional lines book driven by rate below our expectation, smaller average deal size and the continuation of a slower M&A and IPO environment.

Our market-leading business in APAC grew strongly once again, attributable to a broad number of lines of business. Specifically, Australian A&H growth was driven by increased travel volumes, and we benefitted from the first year of production from a newly acquired team of treaty underwriters in Australia and favourable conditions were experienced in Singapore on the reinsurance portfolio.

Net insurance revenue

Net insurance revenue amounted to $2,263.9m compared to prior year of $1,773.9m, 28% higher year on year. The improvement in net insurance revenue is explained by the growth and rate changes described above under insurance contract written premiums.

Insurance service expenses

Insurance service expenses of $2,384.8m capture claims incurred (net of discounting on current year claims), movements on claims incurred in prior periods, acquisition costs and underwriting expenses incurred in the period. This compares to a prior year amount of $1,756.6m.

Against the backdrop of an above average year for total natural catastrophe losses at an industry level, we are pleased to report that our own experience was slightly below our start-of-year expectations, with natural catastrophe losses adding 8.1% (2023:4.6%) to our undiscounted net combined ratio, demonstrating the strength of our risk selection and the quality of our reinsurance programmes. The additional natural catastrophe losses were the major component of an overall 1.5% increase in our undiscounted net combined ratio.

Our current year undiscounted non-cat loss ratio was 44.5% against 43.1% in the prior year. This was driven by strong performance in the UK region of 43.2%, another solid year in APAC, offset by a higher loss ratio in the US and Bermuda. The US and Bermuda region was affected by higher loss ratios in certain classes, though Bermuda performed well. Despite the elevated losses in the US, notably in the second half of the year, the strong overall Group result is testament to the greater diversity and resilience of our business.

The 2023 and prior years have seen improvement in the year with some volatility across classes. Overall prior year development benefited our undiscounted loss ratio by 3.0% as against 1.8% in the previous year.

Our acquisition expense ratio was 27.0% against 29.3% in the prior year. This reduction was largely driven by the growth of our Portfolio Solutions and Reinsurance business lines, where acquisition ratios are lower.

Our underwriting expense ratio in 2024 was 13.5%, stable compared to 13.5% in the prior year. Like in recent years actual expense levels were well controlled in the year, though there was some adverse impact due to the dollar weakening, as much of our expense baFse is in UK Sterling. On an underlying basis our expense ratio is trending down as revenue growth generates operating leverage.

Overall, we recorded a net combined ratio before discounting of 90.2% (2023: 88.7%) and a net combined ratio after discounting of 84.1% (2023: 83.9%). The benefit of discounting of 6.1% (2023: 4.8%) was greater in 2024, primarily due to a slight increase in our average liability duration, reflecting the increased volume of longer-tail reinsurance business. This volatility is out of our control and is why we continue to utilise undiscounted combined ratios for our underwriting management.

Investment return

Total investment return amounted to $193.8m, or 5.4%, compared to a return of $173.1m, or 5.6% in 2023.

We generated $148.9m (2023: $117.4m) of regular investment income, amounting to an income yield of 4.3% (2023:3.8%). Income increased every quarter during the year, as our balance sheet continues to grow.

As expected, the total return benefited from the unwind of mark-to-market losses incurred in prior years as fixed-income securities move closer to maturity, albeit at a lower level than the prior year. We also benefited from some positive fair value gains from slightly narrower credit spreads.

Insurance finance income/expense (IFIE)

The IFIE of $(98.0)m compares to the $(87.0)m in 2023. For 2024, the IFIE comprises $(95.6m) from the unwind of discounting (2023: $(73.5)m) and $(2.4)m resulting from changes in discount rates (2023: $(13.5m)). The higher unwind for the year is primarily the result of growth of the liabilities.

Other operating and administrative expenses

Other operating and administrative expenses increased to $77.3m from $43.6m, with the significant increase being generated from the tax-related item described below.

The major component of other operating and administrative expenses is normal administrative expenses of $50.1m (2023: $43.6m). The increase was because of spending on strategic Group wide initiatives and from a strengthening of sterling compared to the prior year.

Included in the total is an intercompany recharge of $27.2m from our ultimate UK Parent entity (Fortuna Topco Limited) related to additional tax payable under Pillar Two rules on the profits of our Bermudian entities. Under the Pillar Two rules Fortuna Topco Limited is liable for this for this additional tax, however, as it relates to profits generated within the CGL Group, the expense has been recharged to CGL. In 2025, the tax on Bermuda profits will revert to the taxation line, as noted below.

Taxation

The Group tax credit of $8.0m compares to a tax credit of $34.4m in 2023.

In 2024 we have recognised a further UK deferred tax asset of $18.5m (2023: $47.6m) as we expect that tax losses recorded in previous periods will be offset against profits in future. We continue to maintain a sizeable balance of UK unrecognised tax losses.

The current tax in 2024 of $10.5m (2023: $13.2m) comprises charges on overseas taxable profits, except for Bermuda. In 2024, there was a charge pertaining to Bermuda to reflect the new requirements of the Global Minimum Tax (Pillar 2) regime but, in line with the regulations, this was booked in our ultimate holding company and recharged to the Group through an intercompany charge, as referenced above.

From 2025 onwards Bermuda’s new Corporate Income Tax regime takes effect, and any taxes incurred by our Bermudian entities under this regime will be included within the income tax line in CGL’s financial statements. Whilst the liability for any additional tax payable under Pillar Two rules will continue to fall on Fortuna Topco Limited, this is not expected to be material after the introduction of Bermuda’s new Corporate Income Tax regime.

Balance sheet

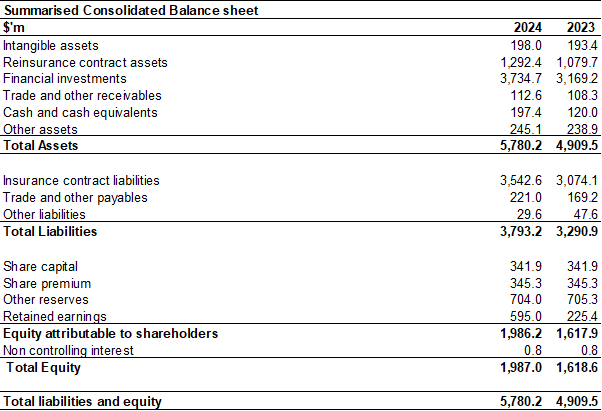

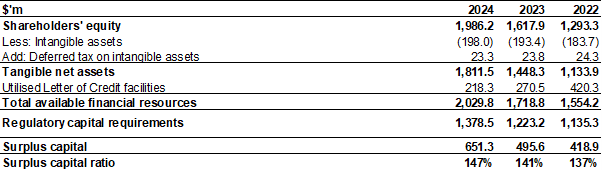

As a result of the Group’s performance during the year our balance sheet is in a very strong position. Shareholders’ equity has increased by 23% from $1,617.9m to $1,986.2m and Tangible Net Asset Value (TNAV) has increased by 25% from $1,448.3m to $1,811.5m.

The Board manages the Group’s capitalisation to ensure that it is appropriate for all the regulatory and rating requirements associated with its medium-term management plan, including maintaining an appropriate amount of surplus for material adverse events and new business opportunities. The Group’s surplus capital is frequently monitored by the Board and is currently maintained at a level above that needed for our internal risk appetite and current regulatory and security rating requirements.

The substantial majority of our capital requirement is driven by the Economic Capital Assessment (“ECA”) at Lloyd’s, which itself is set by Lloyd’s as 135% of the ultimate solvency capital requirement (“uSCR”). The uSCR takes account of one year’s new business in full, attaching to the next underwriting year, and the risks over the lifetime of the liabilities assessed at a 1:200 confidence level (99.5% percentile). The capital requirement of our US balance sheet business is assessed against the US Risk Based Capital (“RBC”) requirements and our Bermuda business is assessed against the Bermuda Solvency Capital Requirement (“BSCR”).

The Group defines it financial resources as the consolidated tangible net asset value of the Group and the utilised portion of its letter of credit (LOC) facility. LOC’s represent only a small part of our financial resources (11%) with the majority represented by tangible net assets. Despite substantial growth in our business, the Group’s capital requirements at 31 December 2024 under the basis described above were $1,378.5m (2023: $1,223.2m). This increase is less than the growth in the Group’s balance sheet and substantially less than the growth in our premium base, primarily because of increased diversification.

This means that our surplus over regulatory requirements was $651.3m (2023: $495.6m), equivalent to a surplus capital ratio of 147% (2023: 141%). This substantial surplus is also considerably in excess of rating agency capitalisation demands at our rating level, providing resilience as well as strategic optionality.

As we are not being regulated at a Group level, we do not prepare a Solvency Capital Requirement (“SCR”) under Solvency II, as many other companies in Europe do. However, the uSCR is more conservative than a one-year Solvency II SCR due to it taking account of all new business and the risks over the lifetime of the liabilities. In addition, as was noted above, the Lloyd’s ECA is also 135% of this more conservative uSCR.

The strength of the balance sheet is underpinned by robust reserving processes. Our positive run-off against our loss picks supports the robustness of the reserves, and we continue to hold a prudent reserve for inflation which has not changed during the year. Our reserves against the Russia/Ukraine war have not materially changed since March 2022, while our claims reserves held against claims relating to the pandemic have reduced following several developments during 2024 that bring more certainty to our loss estimates.

Our net risk adjustment has increased over the course of the year from $108.0m to $126.2m. The confidence interval of the risk adjustment remains unchanged at the 75th percentile and our policy remains to keep this within a range of +/- 2.5%.

On the asset side of the balance sheet, the group remained defensively positioned with 89% (2023: 92%) of investment assets comprising cash, money market funds and core fixed income securities of extremely high quality (73% of our debt and fixed income securities are AAA or AA). We again experienced no credit defaults in our core fixed income portfolio. All of the aforementioned core assets are investment grade, while the total portfolio duration is now 1.2 years (2023: 1.1 years) so as to broadly match the sensitivity of assets and liabilities to interest rate movements.

AM Best reaffirmed the Financial Strength rating of A- (Excellent) in March 2025. The ratings reflect Canopius’ balance sheet strength, which AM Best assesses as very strong. We also continue to benefit from Lloyd’s very strong credit rating.